Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

Language:

Language:

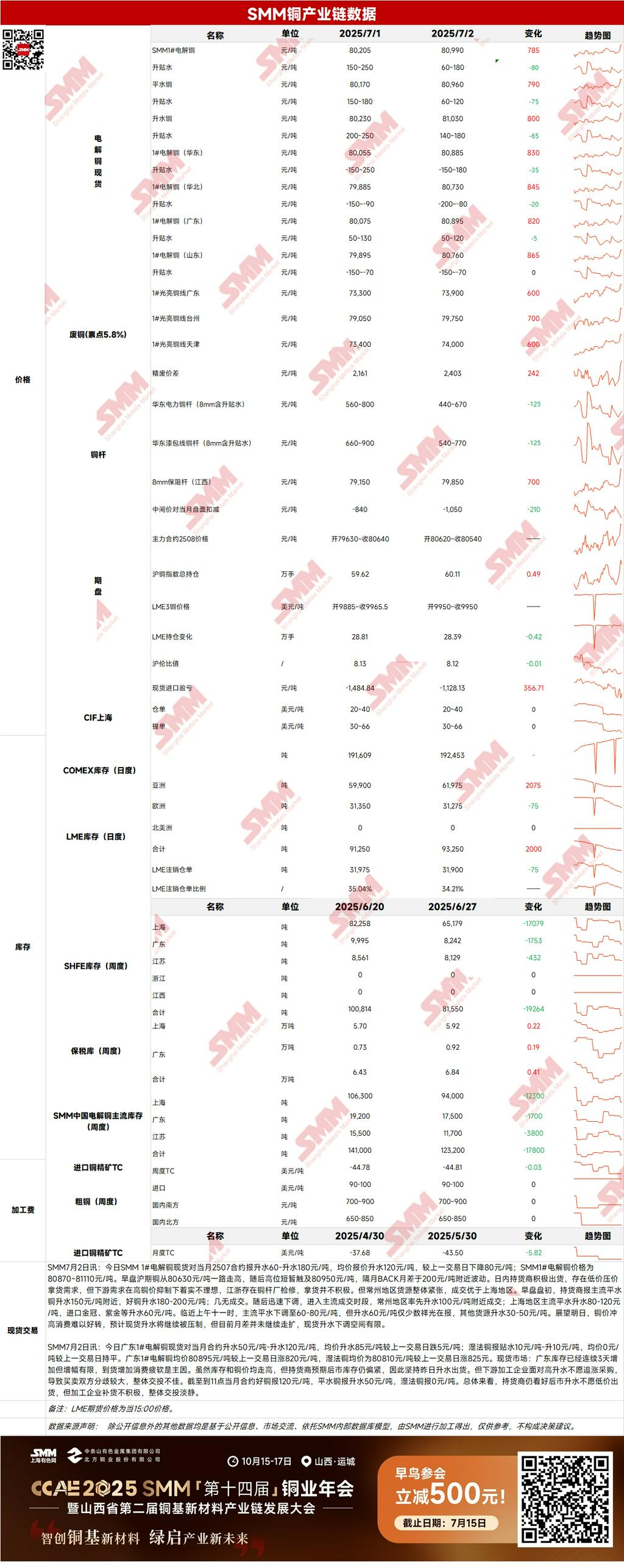

Futures Market: Overnight LME copper opened and dipped to $9,948/mt, then fluctuated upward throughout the session before peaking at $10,020.5/mt near the close. It pulled back slightly to settle at $10,010/mt, marking a 0.67% gain with trading volume reaching 17,000 lots and open interest at 285,000 lots. The most-traded SHFE copper 2508 contract opened and tested 80,560 yuan/mt, fluctuated considerably to peak at 80,990 yuan/mt in early trading, then rebounded to highs after a brief pullback, finally closing at 80,900 yuan/mt with a 0.35% increase. Trading volume reached 36,000 lots and open interest stood at 225,000 lots.

[SMM Copper Morning Briefing] News: (1) MMG's and Hudbay Minerals' Peruvian mines are facing road blockades by informal artisanal miners, disrupting logistics. Copper concentrate shipments from MMG's Las Bambas (projected 380,000 mt in metal content for 2025) and Hudbay's Constancia (projected 80,000-97,000 mt in metal content for 2025) have been suspended.

Spot Market: (1) Shanghai: On July 2, SMM #1 copper cathode spot premiums against the front-month 2507 contract were reported at 60-180 yuan/mt, averaging 120 yuan/mt, down 80 yuan/mt from the previous session. SMM #1 copper cathode prices stood at 80,870-81,110 yuan/mt. Early futures prices rose from 80,630 yuan/mt to briefly touch 80,950 yuan/mt, with the July-August price spread fluctuating near 200 yuan/mt. Looking ahead, while copper prices surge, consumption is unlikely to improve significantly, suggesting continued pressure on spot premiums. However, with the price spread not widening further, downward adjustment space for premiums remains limited.

(2) Guangdong: On July 2, Guangdong #1 copper cathode spot premiums against the front-month contract were 50-120 yuan/mt, averaging 85 yuan/mt (down 5 yuan/mt from the previous session). SX-EW copper was priced at a discount of 10 yuan/mt to a premium of 10 yuan/mt, averaging 0 yuan/mt (unchanged). Guangdong #1 copper cathode averaged 80,895 yuan/mt (+820 yuan/mt), while SX-EW copper averaged 80,810 yuan/mt (+825 yuan/mt). Suppliers remain bullish on future premiums and resist low-price sales, but processing enterprises show weak restocking interest, resulting in quiet overall transactions.

(3) Imported Copper: On July 2, warrant prices were $20-40/mt (QP July), unchanged from the previous session. B/L prices were $30-66/mt (QP July), and EQ copper (CIF B/L) was priced at -$11 to $5/mt (QP July), all unchanged. Pricing references mid-to-late July arrivals. The SHFE/LME price ratio continued improving as LME warehouse data showed increased registered warrant inflows, with initial export cargoes entering warehouses, supporting ratio recovery. Spot offers and transactions increased, but physical premiums showed no improvement.

(4) Secondary Copper: On July 2, secondary copper raw material prices rose 600 yuan/mt MoM. Guangdong's bare bright copper prices stood at 73,800-74,000 yuan/mt, up 700 yuan/mt from the previous trading day. The price difference between copper cathode and copper scrap reached 2,403 yuan/mt, widening by 242 yuan/mt MoM, while the price spread between copper cathode rod and secondary copper rod stood at 1,605 yuan/mt. According to SMM survey, as copper prices resumed upward momentum, secondary copper rod enterprises repeatedly raised procurement prices after morning session quotations. However, rising copper prices intensified suppliers' bullish sentiment, leading to reduced shipments. Secondary copper rod enterprises reported extreme procurement difficulties on the day.

(5) Inventories: On July 2, LME copper cathode inventories increased 2,000 mt to 93,250 mt; SHFE warrant inventories rose 324 mt to 25,097 mt on the same day.

Prices: Macro drivers - US ADP employment fell by 33,000 (vs. expected 95,000), marking the sharpest decline since March 2023. The sluggish labour market showed no signs of improvement, prompting traders to increase bets on at least two Fed interest rate cuts by year-end, forming bullish support for copper prices. Additionally, the US-Vietnam trade agreement reduced planned tariffs on Vietnamese exports, easing trade tension concerns. Fundamentals - Supply side witnessed strong supplier selling willingness, but low-price purchasing pressure emerged amid regional supply tightness in Changzhou. Demand side faced headwinds from elevated copper prices, with rod producers in Jiangsu/Zhejiang reducing purchases due to maintenance shutdowns. Although Changzhou saw relatively active transactions amid tight supply, overall downstream sentiment remained weak. Price outlook - Persisting US economic downward pressure and expanding national debt, coupled with weakened US dollar index, suggest continued upside room for copper prices today.

[The provided information is for reference only and does not constitute direct investment research advice. Clients shall exercise independent judgment and caution, as SMM bears no responsibility for any trading decisions made based on this content.]

For queries, please contact Lemon Zhao at lemonzhao@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn